Blockchain technology has emerged as one of the most transformative innovations of the digital age. While it’s often associated with cryptocurrencies like Bitcoin and Ethereum, the potential applications of blockchain stretch far beyond digital currency. In this beginner’s guide to blockchain technology, we’ll break down the fundamental concepts, how it works, its applications, and why it’s revolutionizing industries across the globe.

What is Blockchain Technology?

At its core, blockchain is a decentralized digital ledger technology that securely records transactions across multiple computers. The key feature of blockchain is that it enables data to be stored in a way that makes it nearly impossible to alter or tamper with. This is accomplished by grouping transactions into “blocks,” which are then linked together to form a “chain.”

Blockchain can be thought of as a distributed database or ledger, where multiple participants have access to the same version of records. This transparency and immutability make it ideal for industries that require high levels of security and trust.

Key Features of Blockchain Technology

Before diving into its applications, it’s essential to understand the core features that set blockchain apart from traditional technologies:

- Decentralization: Unlike traditional systems that rely on a central authority, blockchain operates on a peer-to-peer network, where each participant has equal access to the ledger. This eliminates the need for intermediaries and reduces the risk of fraud or manipulation.

- Immutability: Once a transaction is recorded in a blockchain, it cannot be altered or deleted. This ensures that data integrity is maintained, making blockchain an excellent tool for secure data storage.

- Transparency: Every transaction made on a blockchain is visible to all participants. This promotes accountability and trust, as no one can manipulate the records without others noticing.

- Security: Blockchain uses cryptographic techniques to secure transactions, making it highly resistant to hacking and fraud. This makes it especially valuable for applications involving sensitive information.

How Does Blockchain Work?

To understand how blockchain works, let’s break down the process:

- Transaction Initiation: When a participant (user, organization, etc.) initiates a transaction, it is broadcasted to the network. This could be transferring cryptocurrency, storing a document, or recording data.

- Verification: Before the transaction is recorded, it must be verified by the network. This is done through consensus mechanisms, such as proof of work (PoW) or proof of stake (PoS), depending on the blockchain protocol.

- Block Creation: Once verified, the transaction is grouped with other transactions into a “block.” This block is then added to the blockchain, creating a permanent and immutable record.

- Distributed Ledger: Every participant in the blockchain network has access to the same ledger, ensuring that all parties have the most up-to-date information.

Blockchain Consensus Mechanisms

One of the unique aspects of blockchain is its consensus mechanisms, which ensure that transactions are verified and agreed upon by the network without the need for a centralized authority. Some of the most common consensus mechanisms include:

- Proof of Work (PoW): This mechanism requires participants to solve complex mathematical problems to validate transactions and create new blocks. Bitcoin uses PoW to secure its network.

- Proof of Stake (PoS): In this system, participants validate transactions based on the number of cryptocurrency tokens they hold. Ethereum is transitioning to a PoS model.

- Delegated Proof of Stake (DPoS): This mechanism allows a small number of elected participants to validate transactions, improving scalability and efficiency.

Each consensus mechanism has its pros and cons, but all aim to create a secure, transparent, and decentralized blockchain network.

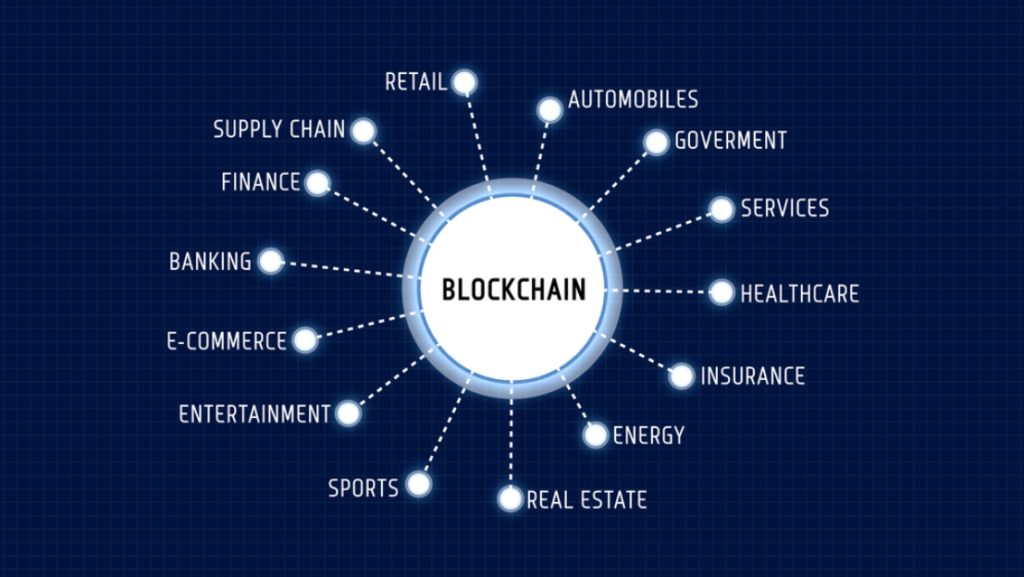

Applications of Blockchain Technology

While blockchain is most famously associated with cryptocurrencies, its applications are far-reaching. Here are some key areas where blockchain technology is making a significant impact:

- Cryptocurrency and Digital Currency: Blockchain is the backbone of cryptocurrencies like Bitcoin, Ethereum, and Ripple. It allows for secure, peer-to-peer transactions without the need for intermediaries like banks.

- Supply Chain Management: Blockchain’s transparency and immutability make it an ideal solution for tracking goods and verifying their authenticity throughout the supply chain. Companies like Walmart and Maersk are using blockchain to improve supply chain visibility and reduce fraud.

- Healthcare: Blockchain can securely store and share patient records, ensuring that medical data is protected while also improving the efficiency of healthcare systems. MedRec is an example of a blockchain-based healthcare platform.

- Voting Systems: Blockchain could revolutionize electoral systems by creating secure, transparent, and tamper-proof voting platforms. With blockchain, each vote would be recorded immutably, reducing the risk of voter fraud and increasing voter confidence.

- Real Estate: Blockchain is being used to streamline property transactions, from recording ownership to simplifying the process of buying and selling real estate. Smart contracts on blockchain could automate the entire property transaction process.

- Smart Contracts: Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically enforce and execute actions when specific conditions are met, making transactions faster, more secure, and cost-effective.

- Digital Identity and Authentication: Blockchain can be used to create secure digital identities for individuals, allowing them to control and verify their personal data. This could help reduce identity theft and improve privacy.

The Benefits of Blockchain Technology

- Increased Security: With encryption and decentralization, blockchain provides enhanced security compared to traditional systems.

- Reduced Costs: Blockchain eliminates the need for intermediaries, which can lower transaction fees and administrative costs.

- Improved Transparency: All transactions are recorded on a public ledger, making it easier for participants to verify and audit actions.

- Faster Transactions: Blockchain allows for faster processing of transactions, particularly in areas like cross-border payments, where traditional methods can take days.

- Decentralization: By removing centralized authority, blockchain provides more control to users, reduces risks associated with single points of failure, and promotes innovation.

Challenges of Blockchain Technology

While blockchain offers numerous benefits, it also faces certain challenges:

- Scalability: Blockchain networks like Bitcoin can be slow and expensive to scale due to their consensus mechanisms. Newer blockchain systems are addressing this with more efficient protocols.

- Energy Consumption: Proof of work consensus, used by Bitcoin, consumes a significant amount of energy, leading to concerns about its environmental impact.

- Regulation: The legal and regulatory landscape for blockchain technology is still evolving. Governments and institutions are working to create frameworks for safe and compliant blockchain applications.

- Adoption: While blockchain has the potential to transform industries, widespread adoption is still in the early stages. Many businesses are hesitant to transition from traditional systems to blockchain-based solutions.

The Future of Blockchain Technology

As blockchain technology continues to evolve, its applications will expand beyond what we can currently imagine. In the future, blockchain could revolutionize everything from financial services and healthcare to government and entertainment. Innovations like Quantum Computing and Interoperability will also play a role in shaping the next generation of blockchain systems.

Also Read: Blockchain Revolution: How Its Transforming Industries Beyond Cryptocurrency

Conclusion

Blockchain technology is more than just the backbone of cryptocurrencies—it is a game-changing innovation that is transforming industries and creating new opportunities for businesses and individuals alike. By providing security, transparency, and efficiency, blockchain is poised to revolutionize the way we store, share, and verify information. As businesses and governments continue to explore and implement blockchain solutions, we will likely see even more innovative applications in the coming years.